The Great Unraveling

Why the Old Tech Business Models No Longer Work

Over a coffee the other day, a friend and I were chatting about ‘the chaos’ that is the current business environment. Today’s environment is more ambiguous that it has been in a long time (as well as being volatile, uncertain, and complex) and this is creating all sorts of challenges in deciding which way to jump.

There’s a lot going on here, but one of the factors that doesn’t get enough attention is how the technology industry (as in IT since the early 1990s) seems to be in transition from a high-margin, high-growth industry, to a low-margin, low-growth one. Looked at through this lens, a lot of trends in the current market make sense. The transition will be compressing margins and flattening revenue, throwing firm operating models out of balance. It is the reaction to this that’s driving a fair chunk of ‘the chaos’ that we’re seeing.

If we want to see where this comes from then we need to step back and consider the longer view. The approach I like, and which I’ve used in the book, is the one used by Richard Baldwin in The Great Convergence.1 This views some aspects of history as a punctuated equilibrium, where long periods of incremental development are interrupted by sudden changes in impact.

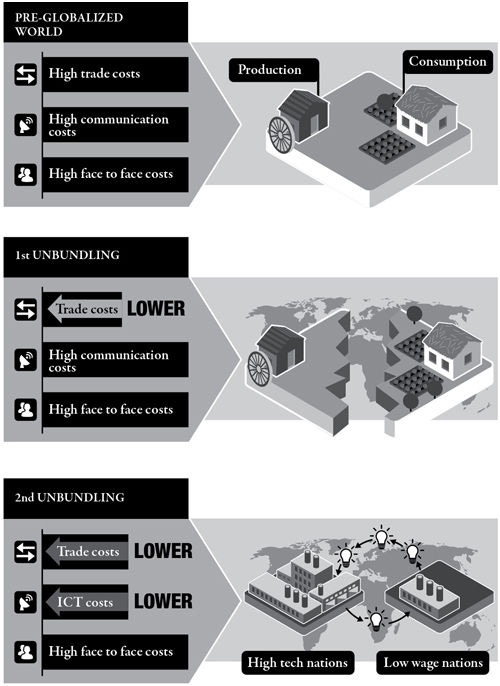

In Baldwin’s case, he broke the history of globalisation into three phases: the pre-globalised world, the first unbundling (roughly 1820-1990), and then the second unbundling (from approximately 1990 onwards). The transition between each phase is facilitated by technology, which comes together in a way that enables us to overcome some constraint, enabling a reconfiguration of institutional relationship that drives us from the present phase to the next. The journey from the pre-globalised world to now is then the story of a series of cascading constraints.

Starting with high trade, communication, and face-to-face costs, the pre-globalised world was one where products were made where they were consumed. The development of steam-powered transportation—particularly steamships and railways—dramatically reduced the cost of moving goods across long distances, collapsing trade costs and enabling production and consumption to be unbundled, with production occurring in one place and consumption in another. The development of modern ICT (information and communications technology, particularly the internet) slashed the cost of coordination, unbundling production itself, resulting in the today’s globalised value chains. Baldwin also predicted a third unbundling,2 when technologies such as VR (virtual reality) and telepresence would collapse the cost of face-to-face interaction to enable telemigration, unbundling the physical presence of workers from jobs, which is playing out now.

Baldwin’s model provides an outside-in view—how changes in the technology landscape are enabling changes in the business environment which, in turn, drives firms to evolve. This explains how technological shifts in the broader environment—especially communication and transportation technologies—enable new forms of global organisation and trade. These external forces then drive firms to adapt their structures and strategies.

The model I’ve developed for Mastering the Puzzles of Transformation (current working title) takes an inside-out view, looking at how firms have been driven to adapt their internal operations to broader changes in the ecosystems they are part of. This focuses on how firms have evolved their internal operations and capabilities in response to changing ecosystem demands, moving through distinct phases as they adapt to new realities.

This inside-out model is built around the observation that incremental adaptation and technology adoption within the firm leads to a point of crisis where it is driven to adopt a new approach, to move to a new ecological niche. Similar to Baldwin’s pre-globalised world, the first phase (‘Phase Zero’) is the pre-digital world, a world of manual processes and paper-based systems. Rather than Baldwin’s cascading constraints, we have cascading complexity: the complexity of coordinating activities within the organisational boundary, of coordinating end-to-end processes that span organisational boundaries, and the complexity of managing relationships, exceptions, and risks in the open market.

In the Phase Zero to One transition, from pre-digital to internal digitisation in roughly 1950, a crisis emerged when manual systems couldn’t handle post-war economic expansion. The response was to adopt computing technology from the military, automating data collation and processing within the firm’s operational silos.

The Phase One (internal digitisation) to Two (closed ecosystems) transition (late 80s or early 90s) was triggered by the personal computer and spreadsheet, as they broke the connections between a firm’s operations, its systems of record, and its reporting obligations. The reporting challenge was addressed by building a layer of software that would synchronise a firm’s various operational systems in real time—a layer of software that is the foundation of modern ERP (enterprise resource planning). The focus shifted to optimising processes, initially within the firm but it was not long before opportunities such as category management were discovered, and processes were optimised end-to-end, across the closed ecosystem that is a firm’s value chain.

Phase Two is currently coming to an end, now in 2024-2025, as we’ve reached the limits of what’s possible via optimising processes. We’ve spent the past 30 years unbundling our monolithic firms, transforming them into closed ecosystems. There’s a crisis brewing though, as firms were no longer just managing internal operations—they are responsible for ecosystem-wide risk and compliance. Data fragmentation across platforms and growing regulatory oversight (ESG, supply chain transparency, etc.) is making process control more complex. Meanwhile, supply chain fragility & exception costs are increasing, making efficiency-focused models unsustainable.

The signs of this brewing crisis are fairly easy to see. Many technology firms—from on-premises EPR vendors through system integrators and cloud-service provides, and even venture capital—are grappling with a market in transition.

Back in the early days, a global ERP rollout took roughly four years. At first these rollouts were driven by compliance, but as vendors discovered more and more process-optimisation opportunities such as category management (or even the whole supply chain boom), value became the driver. At the end of a four-year rollout there was a host of new modules to consider, and these modules provided so much value that you started the whole process again. This created a high-growth, high-margin market.

This story is a bit different today. Decades of unbundling has resulted in a business landscape where firms are, in general, operationally smaller than they were in the past even though revenue continues to increase. There’s also a dearth of new value-driving modules to consider (due to a lack of process optimisation opportunities), causing many firms to push out their ERP upgrade as far as possible, and to descope these upgrades when the do engage with them. Upgrades are further apart and smaller when they do arrive, driving vendors to encourage their clients (often quite strongly) onto subscriptions.

We’re seeing this reality manifest in surprising ways. When a technology company announces “due to the coding productivity benefits of LLMs, we’re not hiring programmers at the moment,” this should not be read as a triumph of efficiency. Rather, it’s effectively saying, “we have a pot of free money but we don’t know what to do with it, so we’re giving it back.” This is a clear sign of a maturing industry—one where companies can no longer productively deploy capital at the same rate they generate it. In high-growth environments, productivity gains quickly translate to new initiatives and expanded capabilities. But in the transition to Phase Three, many firms find themselves generating more capital than they have productive uses for, leading to stock buybacks, dividend increases, and hiring freezes masquerading as technological breakthroughs. This isn’t innovation; it’s the financial management of stagnation.

We can use this model as a lens to look at the entire technology market. Most major enterprise technology companies built their business models around the process optimisation focus of Phase Two—whether it’s ERP systems, supply chain management, CRM (customer relationship management), or integration platforms. The operating models of these companies were designed for the high-margin, high-growth environment that characterised Phase Two, with its regular upgrade cycles and continuous expansion of scope. Even Cloud Computing, which has been the dominant technological shift of the past decade, largely represents an extension of Phase Two thinking—optimising existing processes through different delivery models rather than fundamentally changing the approach. The organisational structures of both technology vendors and their customers have been shaped around a closed ecosystem model, with specialised roles and responsibilities built for managing process optimisation.

This reliance on Phase Two dynamics helps explain ‘the chaos’ my friend mentioned—if we’re truly at the end of what’s possible through process optimisation, then the business models of many technology companies are significantly challenge. It also explains why many incumbent technology companies are struggling to adapt to changing market conditions—their entire organisational DNA is built around Phase Two assumptions.

This framing also sheds a new light on trends such as “Big Data”, which neatly fits neatly into Phase Two. It was positioned as another process optimisation opportunity—collect more data, analyse it better, and uncover new efficiencies and insights. It required significant investment in technology infrastructure and expertise, and promised to extend the high-margin, high-growth dynamics of Phase Two by finding new value in existing processes. While the vendors selling big data tools, platforms, and services did quite well, business-to-consumer Big Data plays have largely failed.3

This pattern of chasing technological silver bullets is playing out across the industry. Bitcoin and cryptocurrency, the Metaverse, and now LLMs (to some extent, as there’s real value there, but also a lot of hype) are all technologies tilting at windmills in the hope of propping up revenue as traditional sources dry up. Each wave follows a predictable cycle: breathless hype about how this technology will “change everything,” massive investment inflows, a scramble to establish market position, and then the gradual realisation that the technology, while potentially impactful, won’t deliver the Phase Two-style growth that investors and executives had hoped for. These cycles represent the industry’s desperate search for new growth engines as the process optimisation well runs dry, attempting to extend the high-margin, high-growth era rather than adapting to the new reality of Phase Three.

It’s not all bad news though. While Phase Two is coming to an end, there’s clearly a Phase Three forming, and it brings new opportunities with it. Phase Three is concerned with Open Ecosystems. Once process integration is widespread, competitive advantage shifts to managing exceptions, disruptions, and emergent opportunities across the ecosystem.4 Value creation shifts from internal process optimisation to external ecosystem coordination and exception management. Firms were no longer just managing their internal operations—firms that excel in managing ecosystem-wide exceptions and disruptions hold the competitive edge.

A good example of this dynamic is supply chains. Phase Two largely solved forward logistics, delivering a product to the point of purchase. Forward logistics is extremely efficient—as we can see with services such as Amazon Prime. Reverse logistics, collecting returns and sorting out what to do with them, is a mess though. It’s where most of the cost is, as returns can come from anywhere, and it’s not clear how they should be processed, or which firms in the value chain are responsible. Returns are a major cost for brands and retailers now. Some are resorting to simply letting customers keep low-value goods—an approach that is likely to be gamed now that it is widely known.

I expect Phase Three to focus on managing value, material, and labour flows across open ecosystems, where firms work together to manage business exceptions and risks. Real value will be unlocked not through more prediction and optimisation within closed ecosystems, but through fundamentally different approaches to organisational boundaries and value creation. Quite a bit of my work over the past few years has focused on identifying opportunities in Phase Three, and it seems that there is the potential to address the productivity concerns that have been building as we’ve come to the end of Phase Two, as well as a wealth of opportunities to create new things.

So ‘the chaos’ is, in part, a consequence of us living in a market in transition. It’s quite possible to manage this transition, though it can be awkward and it means that many firms’ glory days may be in the past. It’s also quite easy to mismanage the transition, and disappear into history.

Baldwin, Richard E. The Great Convergence: Information Technology and the New Globalization. Cambridge, Massachusetts: The Belknap Press of Harvard University Press, 2016.

Baldwin, Richard E. The Globotics Upheaval: Globalization, Robotics, and the Future of Work. Oxford University Press, 2019.

Why AI Is Tech’s Latest Hoax, 2024.

Evans-Greenwood, Peter, and Giselle Hodgson. “Strategy and the Art of the Possible.” Deloitte Insights, July 6, 2022. https://www2.deloitte.com/us/en/insights/topics/strategy/business-ecosystem-strategy.html.

We can add VCs to the list of tech industries that are currently chasing a world that no longer exists.

The viral "Venture Capital is Dead" tweet struck a nerve because the tech sector is fraying. VC funds are posting losses, LPs are pulling back, and the model of rapid exponential returns looks out of step.

This isn't an external disruption story. It's a systemic unraveling from within, driven by the erosion of the foundational assumptions (cheap money, predictable growth) the old "winner-takes-all" tech/VC model was built upon. Even AI, I argue, acts more like a compressor than a savior S-curve in this context.

The current moment demands reinvention in innovation funding – shifting towards persistent, collaborative approaches fit for the world we're in now.